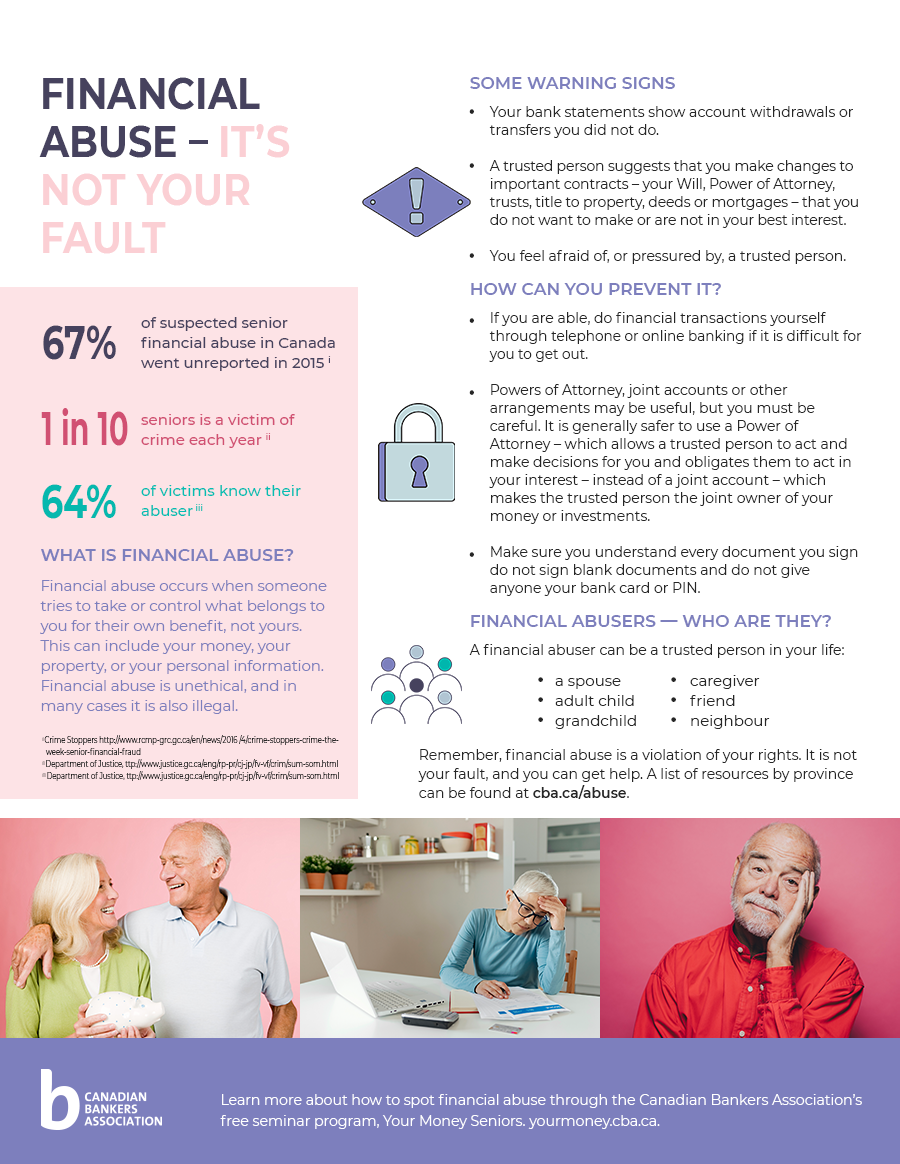

What is financial abuse?

Financial abuse occurs when someone tries to take or control what belongs to you for their own benefit, not yours. This can include your money, your property, or your personal information. Financial abuse is unethical, and in many cases it is also illegal.

Financial abusers — who are they?

A financial abuser can be a trusted person in your life: a spouse, adult child, grandchild or other family member, caregiver, friend, or neighbour.

Examples of financial abuse

A trusted person may be a financial abuser if they:

A trusted person may be a financial abuser if they:

- put pressure on you to give or lend them money, or to give them access to your financial information,

- use a Power of Attorney for their own benefit,

- force or trick you into signing something, including a contract, Will, letter or guarantee,

- take things or money from you without permission,

- misuse your bank card or credit card, or have you take out a loan to help them,

- misuse joint bank accounts or pressure you to make your existing account a joint account,

- forge your signature on cheques, including pension cheques, or legal documents,

- sell or transfer your property against your wishes or interests, or

- refuse to return borrowed money or property.

Some warning signs

- A trusted person takes an undue interest or involvement in your financial matters.

- Your statements show account withdrawals or transfers you did not do.

- A trusted person suggests you have your bank statements sent to them (or you stop receiving your bank statements).

- You start failing to meet your financial obligations, when you’ve never had problems before.

- A trusted person suggests that you make changes to important contracts – your Will, Power of Attorney, trusts, title to property, deeds or mortgages – that you do not want to make or are not in your best interest.

- You feel afraid of, or pressured by, a trusted person.

How can you prevent it?

If you are able, do financial transactions yourself. Take advantage of telephone and online banking if it is difficult for you to get out.

When planning for your possible inability to manage your finances yourself, allowing a trusted person (or persons) to assist with your financial affairs can be helpful, but you must select your trusted person carefully.

Powers of Attorney, joint accounts or other arrangements may be useful, but you must be careful. It is generally safer to use a Power of Attorney – which allows a trusted person to act and make decisions for you and obligates them to act in your interest – instead of a joint account – which makes the trusted person the joint owner of your money and investments. Read more about these tools in Powers of Attorney: What Consumers Need to Know, Powers of Attorney: Bank Requirements, Powers of Attorney: Opening a Bank Account with a Power of Attorney, and Joint Accounts: Appropriate Use of Joint Accounts on the CBA website.

You can say “no” when someone pressures you for money or to buy something — even family members.

Make sure you understand every document you sign – do not sign blank documents and do not give anyone your bank card or PIN.

You can have pension cheques, or other sources of income, deposited directly into your bank account and have your bills debited directly out of your account or charged to your credit card.

Where to get help

Remember, financial abuse is a violation of your rights. It is not your fault, and you can get help. Click here for contact information by province/territory.

Please consider obtaining legal advice for all matters related to POAs and planning for incapacity. This text only provides general information and does not constitute a legal opinion. Since the POA rules vary between provinces, the CBA strongly encourages you to seek advice from a legal expert before making any decision in these matters.

Did you know?

Did you know?

The CBA offers a free fraud prevention seminar for seniors as part of its Your Money Seniors financial literacy seminar program. Request a fraud prevention seminar today!